Rising Unemployment in the UK

Summary

-

Panellists were mixed on the balance between structural and cyclical factors explaining the recent rise in unemployment. Half of the panel (47%) thought rising unemployment was best explained by an increase in the long-run unemployment rate, while 32% of the panel thought it was best explained by cyclical weakness in demand. The remaining 21% viewed the impact of both factors as roughly equal.

-

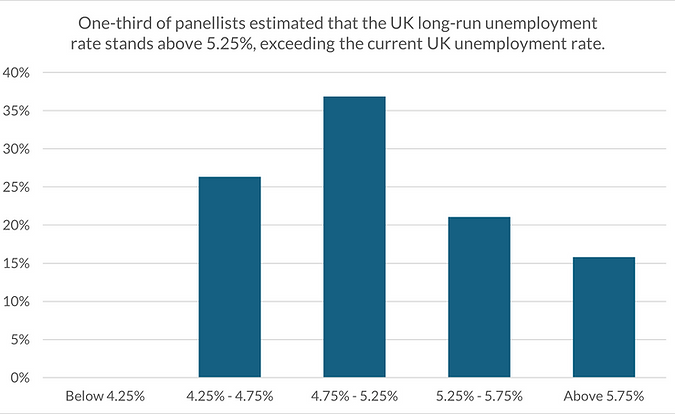

One-third of panellists estimated that the UK long-run unemployment rate stands above 5.25%, exceeding the current UK unemployment rate. A further third of the panel placed the rate between 4.75% and 5.0%, while 25% estimated it between 4.25% and 4.75%. No panellists proposed a rate below 4.25%, placing the entire panel above the OBR’s latest forecast of 4.1%.

-

Half of the panel (47%) identified government policies as a very important driver of the rise in young NEETs and youth unemployment over the past year. A further 32% of panellists considered these policies a moderately important factor, while 21% viewed them as not very important.

Question 1: To what extent is the recent rise in unemployment best explained by a rise in the UK’s long-run level of unemployment, rather than cyclical weakness in demand?

Nineteen panellists responded to this question. Half of the panel (47%) thought rising unemployment was best explained by an increase in the long-run unemployment rate, while 32% of the panel thought it was best explained by cyclical weakness in demand. The remaining 21% viewed the impact of both factors as roughly equal.

Several panellists emphasised the role of government policies in driving UK unemployment. Michael Wickens (University of York) argued: “The rise in unemployment is almost entirely due to government policy. Reduced demand due to higher taxes. Lower employment demand due to higher business taxes, higher labour taxes, higher minimum wage, higher energy costs, the disappearance of growth and the adoption of AI. On top of this additional welfare support and the hangover from Covid has discouraged labour force participation. A perfect storm and it will get worse under this government.”

Structural shifts emanating from AI adoption and long-term health problems were cited by the panel. Ricardo Reis (LSE) commented: “Not many indicators points to any cyclical weakening of demand, while there are many technological changes that can plausibly affect the long-run level.” Ethan Ilzetzki (LSE) highlighted structural trends in younger cohorts: “The share of youths not in education, employment, or training has risen steadily since the Covid-19 pandemic and five years on, it is difficult to see this as merely a cyclical phenomenon. The main underlying factor appears to be the increase in youths not seeking employment because of disability or health.”

The effects of Brexit were also mentioned. Lucio Sarno noted: “There is a possibility the negative long-run growth shock due to Brexit may have increase structural unemployment. However, this is likely to be offset but lower future immigration, resulting in roughly equal long-run unemployment levels.” Matthias Doepke (LSE) took a structural view of rising unemployment and attributed the rise in the long-run level to “Brexit, low productivity growth, persistent decline in investment”.

Question 2a: What is your best estimate of the UK long-run unemployment?

Nineteen panellists responded to this question. One-third of panellists estimated that the UK long-run unemployment rate stands above 5.25%, exceeding the current UK unemployment rate. A further third of the panel placed the rate between 4.75% and 5.0%, while 25% estimated it between 4.25% and 4.75%. Notably, no panellists proposed a rate below 4.25%, placing the entire panel above the OBR’s latest forecast of 4.1%.

Question 2b: How confident are you in your answer?

Nineteen panellists responded to this question. Half of the panel reported being "moderately confident," while one-third were "not very confident" and 16% were "not confident at all". None of the panel were “very confident” in their judgements.

No clear pattern emerged regarding the distribution of confidence across different rate estimates; however, all three respondents who estimated a long-run rate above 5.75% were "moderately confident" in their assessments.

Question 3: IHow important have recent government policy changes (including higher employer NICs and the National Minimum Wage) been in explaining the increase in young NEETs/young joblessness over the past year?

Nineteen panellists responded to this question, with half (47%) identifying government policies as a "very important" driver of the rise in youth unemployment and NEET rates over the past year. A further 32% considered these policies a "moderately important" factor, while 21% viewed them as "not very important". No panellists categorised government policy as "not at all important".

Panellists highlighted that the simultaneous rise in NICs and the NLW meant that firms adjusted by squeezing employment rather than by reducing wages. Charles Bean (LSE) noted: “For high-wage labour, the empirical evidence suggests that the burden of higher employer NI would eventually be passed back onto workers through lower real wages. However, that is difficult to achieve if pay is already close to the minimum wage, although some of the higher costs may instead still be recouped through higher prices.” James Smith (Resolution Foundation) made a similar observation: “The NI/ NLW changes have interacted in a way that means the adjustment has come through lower employment (rather than through wages). This effect is larger at the bottom end of the labour market, which disproportionately affects younger workers, and for that group this is exacerbated by larger rises in youth minimum wage rates.” Ricardo Reis (LSE) cautioned that while “government policy changes are the most likely proximate cause for such large movements in young joblessness… the evidence is very far from being strong”.

A number of panellists argued that the interaction of government policies with cyclical factors was important. Paul Mortimer-Lee (NIESR Fellow) commented: “When the labour market is slackening, the pool of previously employed experienced workers available for a job rises. The probability of a firm hiring an inexperienced worker with fewer general or job specific skills falls. So the cycle is part of the explanation. If the young person’s costs rise relative to those of an experienced worker, the incentive to hire a new entrant drops further. These policy changes are not what you should be making in a downturn.” David Cobham (Heriot-Watt University) emphasised weak demand as the driver of unemployment trends: “Complaints about NICs and the NMW are easy avenues for businesses facing difficulties, but those rises would be well outweighed by demand increases if there was some kind of take-off.”

Panellists also pointed out future risks to youth unemployment. Nicholas Oulton (LSE) commented that rising youth unemployment may reflect “firms' anticipation of future changes going in the same direction, such as the abolition of the youth rate of the National Minimum Wage” but qualified his judgement with “doubts about the basic measurement of unemployment, which comes from the deeply problematic LFS.” While acknowledging the importance of government policies, Roger Farmer (University of Warwick) highlighted the unemployment risks posed by AI: “The main reason for being pessimistic about the trend in the unemployment rate is the likely effects of AI on the labour market that will be hitting in the next one to two years. My best guess is that many job openings that had previously been available to graduates and or school leavers are about to be replaced by AI. The transition a new economy is likely to be highly disruptive.”

To access the full panel responses, including the free text comments where respondents expanded on their answers, please download this MS Excel sheet.