Post Covid-19 Potential Output in the Eurozone

Ethan Ilzetzki[1]

Wednesday, 16 December, 2020

Summary

A majority of the CfM-CEPR panel of macroeconomic experts on the European economy predict a 2-5% decline in the level of potential Eurozone GDP, but no impact on potential the long-run growth rate.

Background

The December 2020 CfM-CEPR survey asked members of its European panel to estimate the loss in the level and growth rate of potential GDP in the Eurozone due to the Covid-19 pandemic.

Covid’s Long-run Impact on the Eurozone Economy

Global economic activity took a large hit during the Covid-19 pandemic. The Eurozone is no exception with the European Central Bank (ECB) currently projecting an 8% decline in GDP this year and that GDP will only recover to its pre-pandemic level at the end of 2021. But looking five years ahead, the ECB has made no change to its long run growth forecast (of 1.4% in five years’ time) throughout the pandemic. This particular forecast suggests a permanent loss in the level of GDP, but no effect on its growth in the long run. Yet, the long run effect of Covid-19 on the Eurozone’s economic potential remains very uncertain.

Bodnár et al. (2020) give an overview on the theory and evidence on the effects of Covid-19 on the Eurozone’s potential output. Potential output is defined as the maximal level of economic activity that an economy can sustain at current technology, labor supply, and capital stock, without leading to inflationary pressures. There are several reasons to think that Covid-19 may have persistent effects.

First, supply chain disruptions can cause a decline in the economy’s productive capacity, but how persistent these are is still uncertain. Vinci and Licandro (2020) point out the role of monetary policy interventions in preventing the destruction of productive capacities following large negative shocks. Second, it may take time for new entrants to replace firms that failed due to Covid-19. Third, unemployment tends to be persistent as workers’ skills deteriorate and their attachment to the labor force may weaken. Fatás and Summers (2017) give evidence of hysteresis effects of this sort.

Fourth, corporate debt overhang may create “zombie firms”, who have lesser incentives to invest in productive capital. However, Jordá et al (2020) find no historical support for post-crisis growth depending on corporate debt levels. Fifth, there is some theoretical support to the notion that low demand may have scarring effects on the economy due to underinvestment in capital or innovation, whether the recession originated from the demand or supply side (Benigno and Fornaro, 2018; Fornaro and Wolf, 2020; Benedetti-Fasil et al, 2020). Finally, pessimistic forecasts of long run growth can be self-fulfilling because policymakers are more likely to enact fiscal consolidation if they foresee a permanent loss in output. This, in turn, could secure the drop in GDP due to lower demand (Heimberger, 2020).

There are also reasons why Covid-19 may increase the economy’s long-run growth potential. It may have accelerated the implementation of new technologies. Further, it has and could lead to improvements in health investments.

It is difficult to come by forecasts of the long-run economic damage caused by Covid-19. Pujol (2020) evaluates private sector forecasts and summarizes that they point to expectations of a permanent loss of 3-4% in the level of GDP, with large variation across countries. The European Commission estimates that German and French potential GDP have both declined by half a percent in the years 2020-21. The commission doesn’t attempt to forecast long-run potential economic growth and instead assumes no effect on long run growth. The World Bank’s Global Economic Prospects (June 2020) forecasts that the Eurozone will not regain pre-Covid levels of GDP until the second half of 2023. The UK Office of Budget Responsibility forecasts a permanent 2 percent loss in UK productivity and a 1 percent decline in the labor supply, amounting to a 3 percent drop in the level of potential GDP. But this too is forecasted to be a drop in the level of potential output rather than its trend and the forecast has a large range of scenarios ranging from 0% to 6%. NIESR forecasts a broad range of outcomes across countries, with fiscal support during the crisis being the main factor determining how well a given economy recovers.

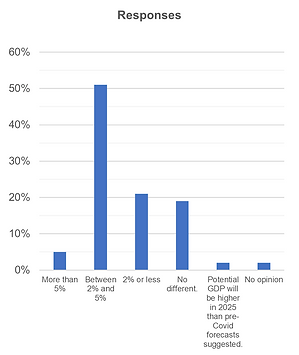

Question 1: How much lower will the potential level of GDP in the Eurozone in 2025 be due to Covid-19 relative to pre-Covid forecasts?

Forty-three panelists responded to this question. A majority (51%) of the panel predicts that the level of potential GDP will be 2-5% lower in 2025 than it would have otherwise been absent Covid-19. In other words, they predict a permanent loss in income due to Covid. However, nearly 40% of the panel predicted a small or negligible cost in terms of the level of GDP, with 21% predicting that potential GDP will decline by 2% or less, and 19% that it will not decline at all.

The more pessimistic responses note that GDP losses in deep recessions tend to be permanent. Roger Farmer (University of Warwick) points out that “After a major shock, and COVID certainly qualifies as major, there is little or no tendency to return to a give[n] path.” Several participants pointed to factors that were unique to Covid-19 and may have a longer-term effect. David Miles (Imperial College) referred to the “Education disruption and failure of firms allied with a sharp rise in unemployment” as factors affecting the economy in the long run. Francesco Lippi (LUISS) highlights other scarring factors including “higher public and private debts [and] more unemployment.” Other respondents voiced concern that political and social factors may further hamper the recovery. Etienne Wasmer (Sciences Po) argues that “This is a break in the trend, and Europe has traditionally be[en] slow to adjust to a new organization, it will indeed take 5 to 10 years to adjust.” Ramon Marimon (European University Institute and UPF-Barcelona GSE) points directly to EU politics: “The main problem is not the potential level in the Eurozone in 2025, but how the Eurozone divide, which already increased after the financial-euro crisis, will be in 2025?”

The optimists noted that Covid-19 may also be viewed as a creative destruction shock. Francesco Lippi, while noting the risks of scarring effects above, believes potential GDP could be higher because “The shock pushed many firms to adopt new technologies that may be cost effective in the medium run and increase potential output and welfare.” Robert Kollmann (Université Libre de Bruxelles), while predicting a minor loss to long run GDP, adds that “households and firms have been forced by the Covid crisis to upgrade their IT skills and equipment, and new ways of organizing office work, production and distribution have been invented. In addition, the crisis could accelerate the transition to greener technologies.” Others credit good macroeconomic policy to their rosier forecasts. John Hassler (IIES, Stockholm University) predicts that “Most likely, the fundamental cause of the crisis will vanish this year. Due to very forceful policies, the initial shock did not lead to self-reinforcing feedbacks – a quite possible scenario with a financial crisis leading to perhaps even a depression was avoided.” However, Thorsten Beck (Cass Business School) warns that the outcome depends on future policies as well: “The impact of COVID-19 on potential GDP will depend a lot on policy responses. So far, these policy responses have been appropriate, trying to minimise negative effects. But political doubts remain whether they can be continued long enough to avoid damage.”

Finally, several panel members argued that the Eurozone should not be viewed as a single economy and that there will be large differences across countries in the pace of recovery. Jagjit Chadha (National Institute of Economic and Social Research), for example, points to “considerable heterogeneity across EA countries because of their respective reliance on socially intensive activities, the scope for available fiscal responses and the effectiveness of the health and social care infrastructure.”

Question 2: How much lower will the potential growth rate of GDP in the Eurozone in 2025 be due to Covid-19 relative to pre-Covid forecasts?

Forty-seven members of the panel responded to this question. The vast majority (81%) predicted that the Eurozone’s potential growth rate will be unaffected by Covid-19 or forecasted small losses of half a percentage point or less.

Some panelists based their responses on past recessions. Jumana Saleheen (CRU Group) reminds us that “In previous crisis we have seen an impact on the level of potential GDP but not on its growth.” Other panelists argued that none of the long-run drivers of economic growth have been adversely affected. As Jordi Galí (CREI, Universitat Pompeu Fabra and Barcelona GSE) puts it: “I do not see any reason to believe the forces behind innovation and, hence, potential growth, will be much different after the pandemic, one way or another.” John Hassler adds: “It is hard to see that the fundamental causes of growth, namely the creation of new ideas and the ability to adopt and exploit these for commercial and social use, are affected in the long-run by the coronacrisis.”

A couple of participants were even more optimistic. Fabrizio Coricelli (Paris School of Economics) argues that Covid-19 will end up being good for economic growth: “Covid-19 may induce much needed infrastructural public investments, speed up productivity enhancing technological innovation, also driven by environmental concerns.” Maria Demertzis (Bruegel) adds: “There are important reasons to [feel] that new technology adaption has been accelerated as a result of Covid-19.”

However, several participants warned that these optimistic forecasts depend on the policy response. Etienne Wasmer conditions that “if we are in the middle of [a] public finance crisis, it will be a -2 to -3% [hit to GDP growth], but [it’s] hard to tell whether this is in 2025, 2024 or 2023.”

References

Benedetti-Fasil, Cristiana, Giammario Impulitti, Omar Licandro and Petr Sedlacek, “Heterogeneous Firms, R&D Policies and the Long Shadow of Business Cycles,” unpublished manuscript

Benigno, Gianluca and Luca Fornaro, “Stagnation traps", The Review of Economic Studies, 2018

Bodnár, Katalin, Julien Le Roux, Paloma Lopez-Garcia and Bela Szörfi, “The impact of COVID-19 on potential output in the euro area”, ECB Economic Bulletin, 2020

Fatás, Antonio and Lawrence H. Summers, “The Permanent Effects of Fiscal Consolidations,” Journal of International Economics, 2017.

Fornaro, Luca and Martin Wolf, “Covid-19 Coronavirus and Macroeconomic Policy: Some Analytical Notes”, manuscript, 2020

Heimberger, Philipp, “Potential Output, EU Fiscal Surveillance and the COVID-19 Shock”, 2020

Jordà Òscar, Martin Kornejew, Moritz Schularick and Alan M. Taylor, “Zombies at Large: Corporate Debt Overhang and the Macroeconomy,” CEPR discussion paper DP15518, 2020.

Pujol, Thierry, “The Long-Term Economic Cost of Covid-19 in the Consensus Forecasts,” Covid Economics 44, CEPR, 2020.

Vinci, Francesca and Omar Licandro “Switching-track after the Great Recession,” CFCM Working Paper 02/2020.

[1] The author acknowledges Jason Jia for his able research and editorial assistance.